Robust Capital Allocation in an Uncertain Energy Landscape

In previous Insights, we have discussed how economic viability is increasingly determining which energy-efficiency measures are implemented, how portfoliomodelling enables comparability between investments, and how risk and robustness influence profitability both in individual buildings and across entire property portfolios. However, risk analysis only acquires real value when it influences how investments are prioritised and how property portfolios evolve over time.

The question therefore becomes strategic: how can an investment strategy be created that remains robust even when the future is uncertain?

Strategy Is About Prioritisation Under Uncertainty

Strategic decisions are almost always made under uncertain conditions. This very much applies to investments in energy efficiency as well. Energy prices change, capital costs fluctuate, technology evolves, and future requirements for buildings are difficult to predict in detail.

At the same time, access to capital is limited. Energy-efficiency investments compete with other investments such as maintenance, tenant adaptations, upgrading standards, and new construction. Strategy is therefore not about identifying individual measures with the highest possible theoretical return, but about prioritising investments in a way that provides long-term stability in the economics and functionality of the property portfolio.

This means that the “most profitable” measure is not always the most strategically sound one. An investment that depends heavily on favourable energy prices or low discount rates may appear attractive in calculations while at the same time contributing to increased vulnerability across the portfolio as a whole. One example could be extensive building envelope measures with very long payback periods. If energy price developments prove weaker than expected while capital costs rise, the same investments may tie up large amounts of capital for a long period without delivering the expected economic effect. A property portfolio dominated by this type of investment therefore risks becoming less financially flexible.

Ultimately, strategy is therefore about making decisions that remain sustainable even when future conditions change.

From Individual Measures to Investment Policy

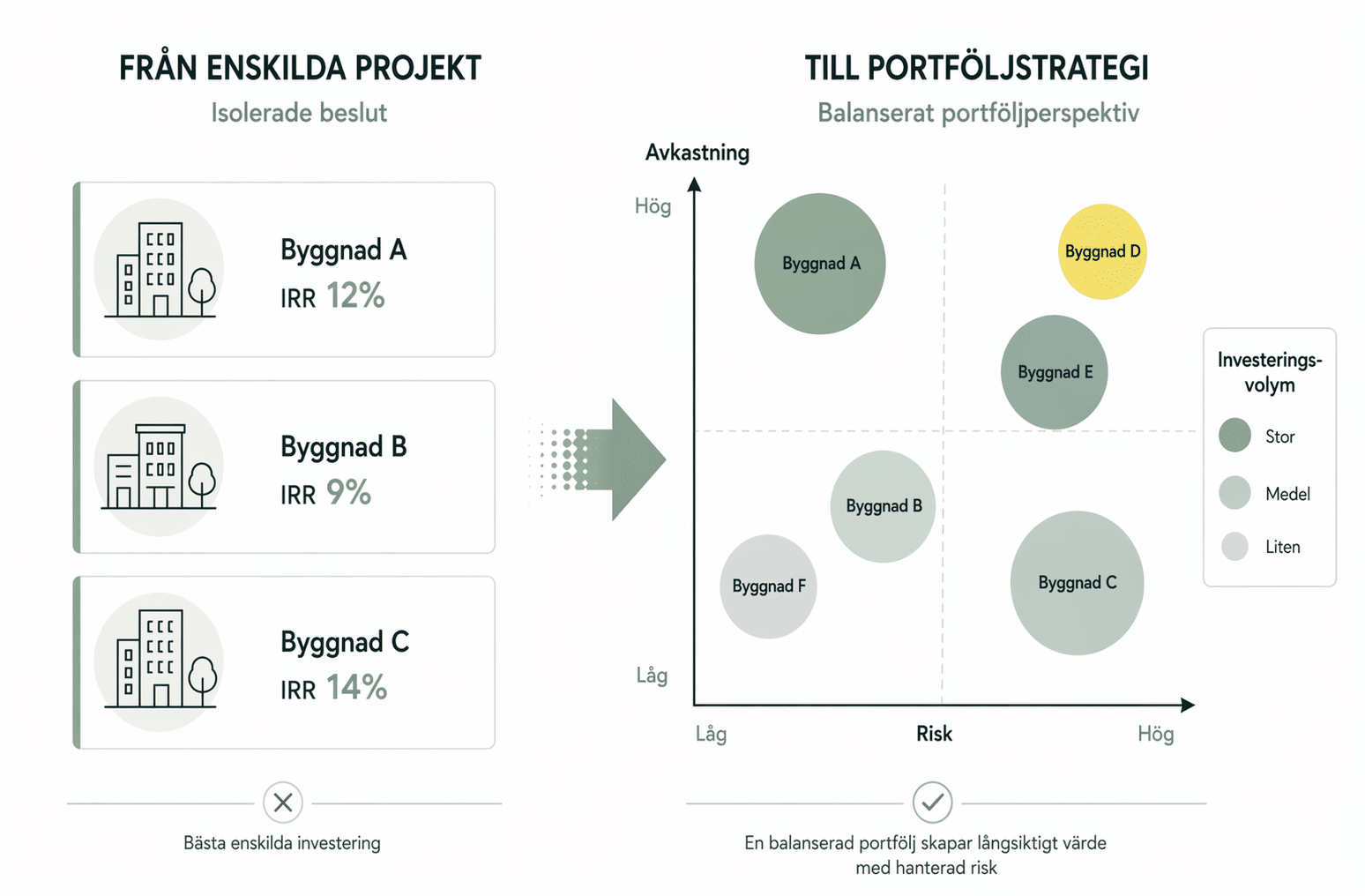

In many organisations, energy efficiency is still treated as a series of separate projects. Measures are identified building by building and prioritised on the basis of individual profitability. Such an approach risks creating a fragmented investment pattern in which the broader perspective is lost.

When the risk perspective is integrated, the analysis changes. The focus shifts from the question “Which measures should be implemented?” to the question “What types of investments should dominate the portfolio over time?”

This opens the way for a more strategic investment policy. Robust measures with stable returns can form a long-term foundation for energy work, while more uncertain investments are implemented more selectively and under conditions where the level of risk is acceptable.

In practice, this is often about trade-offs rather than optimal solutions. A property company may, for example, choose to combine robust and relatively low-risk measures with more uncertain investments offering higher potential returns. Similarly, extensive long-life investments may need to be weighed against smaller measures that provide greater future flexibility. Strategic energy work is therefore less about maximising individual calculations and more about creating balanced development across the entire portfolio.

In this way, energy efficiency ceases to be a collection of isolated projects and instead becomes an integrated part of the property company’s strategic management and capital allocation.

Time Horizons Change the Strategy

The time perspective is crucial in strategic energy investments. Many measures affect the energy performance of buildings for several decades. At the same time, uncertainty regarding future energy prices, technological development, and capital costs is considerable.

This means that investments should not be assessed solely on the basis of today’s economic conditions. A measure that appears optimal in a short-term perspective

may prove less robust over the longer term, particularly if it restricts future flexibility or is based on overly specific assumptions regarding market developments.

In this context, flexibility acquires strategic value. The possibility of gradually developing buildings and technical systems may in some cases be more important than maximising short-term calculated returns. One example could be ventilation or control systems that are expanded step by step and can be adapted to future technological developments, rather than very large investments that lock the building into specific technical solutions for a long period. Similarly, gradual improvements to the building envelope and installations may sometimes provide greater strategic flexibility than a major one-off investment optimised for today’s conditions.

The most profitable measure today is therefore not necessarily the most strategically robust over time.

Robustness as a Strategic Principle

As uncertainty increases, the meaning of successful energy work also changes. The focus gradually shifts from maximum optimisation to robustness, which in this context means maintaining reasonable functionality, financial performance, and flexibility even when future conditions change. Strategic energy work is therefore less about maximising individual calculations and more about creating a property portfolio with long-term robust economics and operational flexibility.

In practice, this means that investments must be evaluated not only on the basis of expected returns, but also in terms of how sensitive they are to changes in energy prices, interest rates, and other key assumptions.

Robustness thus becomes not a side effect of energy efficiency, but a strategic characteristic of capital allocation itself.

Portfolio Modelling as a Management Instrument

From this perspective, the role of portfolio modelling also changes. It is no longer solely about analysing or comparing investments. Instead, the ability to provide a basis for long-term management becomes crucial.

When the entire portfolio is analysed within the same technical and economic framework, it becomes possible to study how different investment strategies affect risk, cash flow, and robustness over time. Scenarios can be compared, and the

consequences of different priorities can be made visible before investments are implemented.

This means that energy work can increasingly be integrated into the property company’s overall strategic planning. Energy efficiency then becomes not a separate technical issue, but part of the company’s long-term development of value, risk, and capital structure.

In this context, the calculation platform evolves from an analysis tool into a management instrument. The development of BIM Energy in recent years also reflects this shift – from an almost purely technical calculation tool into an increasingly strategic analytical support system for scenario analysis, portfolio modelling, and long-term capital allocation.

From Optimisation to Long-Term Direction

The energy work of the future will probably focus less on identifying individual profitable measures and more on building property portfolios that are robust against changing economic and technical conditions.

Robustness is therefore ultimately not about calculations. It is about the ability to make sustainable decisions despite an uncertain future.

Profitability determines what can be done. Strategy determines what should be done.